Revenue Growth and EBITDA Multiple Expansion Drove Historical Health Care Investment Returns

Will Future Return Components Mirror the Last Decade?

During 2021, private equity funds and strategic buyers deployed a record amount of capital into health care businesses. Investors’ perception of stable profit margins and a recession-resistant profile encouraged new participants to enter the space, pushing up valuations and intensifying competition.

To understand investor interest and strategy, it is important to understand the underlying drivers of return generation. Over the last decade, transactions of health care private equity portfolio companies have occurred in a very strong market with expectations of revenue growth and EBITDA multiple expansion, which, somewhat circularly, is encouraged by past performance and achievements.

By the Numbers

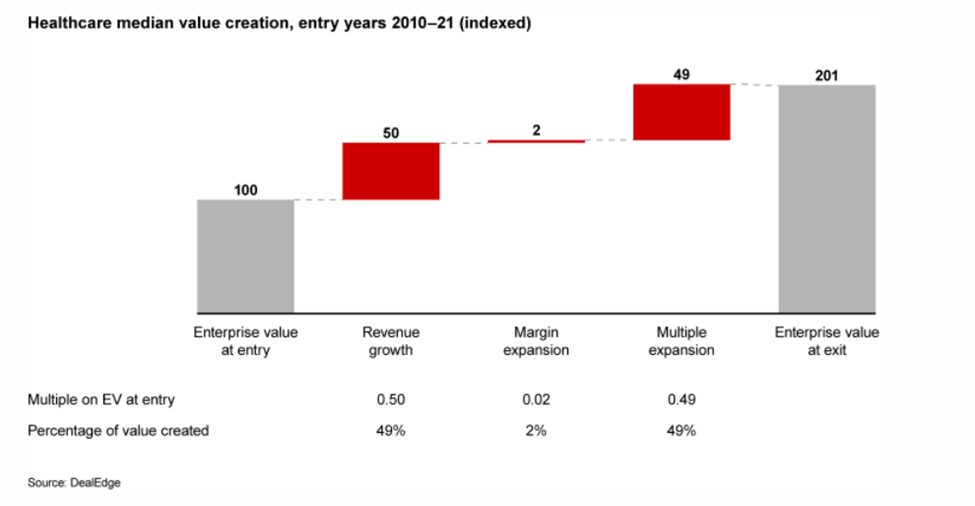

As illustrated in the chart below by Bain Capital, revenue growth and EBITDA multiple expansion have contributed equally to expansion of enterprise value at exit over the last decade (2010-2021) as relates to health care enterprises. According to Bain Capital, the resulting median compound annual revenue growth rate for health care was 11.1% compared to 7.6% for all other industries. Changes to EBITDA margins was neither a positive nor negative contributor to value creation over this period, as this metric largely held stable.

*Click to enlarge the image below.

Source: Bain Capital

Why It Matters

In the next ten years, factors affecting investor returns in health care may be different compared to the prior decade. Going forward, investor expectations will be influenced, in part, by the following:

- Rapidly rising labor and supply costs combined with tepid pricing growth expectations will likely negatively affect the margin expansion return component and the multiple expansion component.

- Exit EBITDA multiple growth may be harder to achieve in the future as enterprise value at entry continues to rise while profit margins contract.

Health Care Valuation Takeaways

- Health care companies are finding new streams of revenue through geographic expansion, new technologies and consolidation. There is high likelihood that revenue growth will continue due to the continued consolidation of a highly fragmented health care market.

- As deals become more competitive and entry multiples rise further, it is likely that revenue growth component will become the most important – and perhaps the only – source of investment return value.

- If we expect margin contraction due to higher and enduring labor costs, lower profit margins may become a negative return component. Contracting margins may also negatively influence the multiple expansion component, once again leaving only revenue growth as the sole component to value creation over the next decade.

- The valuator needs to determine if the transaction return components from the last decade will mirror those of the next decade and, if necessary, make appropriate adjustments to valuation assumptions.

Dig Deeper

For information about health care provider valuations, contact us. We are here to help.

© 2022

This is one in a series of related health care valuation posts:

- Surgery Outmigration Driving Elevated Valuation Multiples in the ASC Segment

- Increased Contract Labor Costs May Lead to Valuation Revisions

- Expanding Supply of Urgent Care Centers Create FMV Considerations

- Behavioral Telehealth Growth May Mean Opportunities for Inpatient Operators

- The Future of US Health Care Profits

- Hospital Expense Statistics Illustrate Significant Labor Pressures

- Hospital Earnings Supported by Fewer Uninsured Patients

- Health Care Services Transaction Volume Declines Below Pre-Pandemic Levels